Why is gold falling even with war and inflation?

My read is that gold's problem is not the absence of inflation. It is the wrong kind of inflation colliding with still-high real rates. Gold typically benefits most when real yields fall, policy expectations get easier, and the dollar softens. The current shock is different. The February 28, 2026 U.S.-Israeli strikes on Iran and the retaliation that followed pushed oil higher, which raises the risk of stubborn headline inflation without necessarily delivering the easier monetary backdrop that gold usually wants.

That is why the metal can look strangely weak in the middle of geopolitical stress. A supply shock can keep central banks boxed in, hold real yields up, and force investors to de-risk elsewhere. When that happens, gold stops behaving like a clean inflation hedge and starts looking like a crowded macro trade with vulnerable positioning.

| Metric | Latest reading | Why it matters |

|---|---|---|

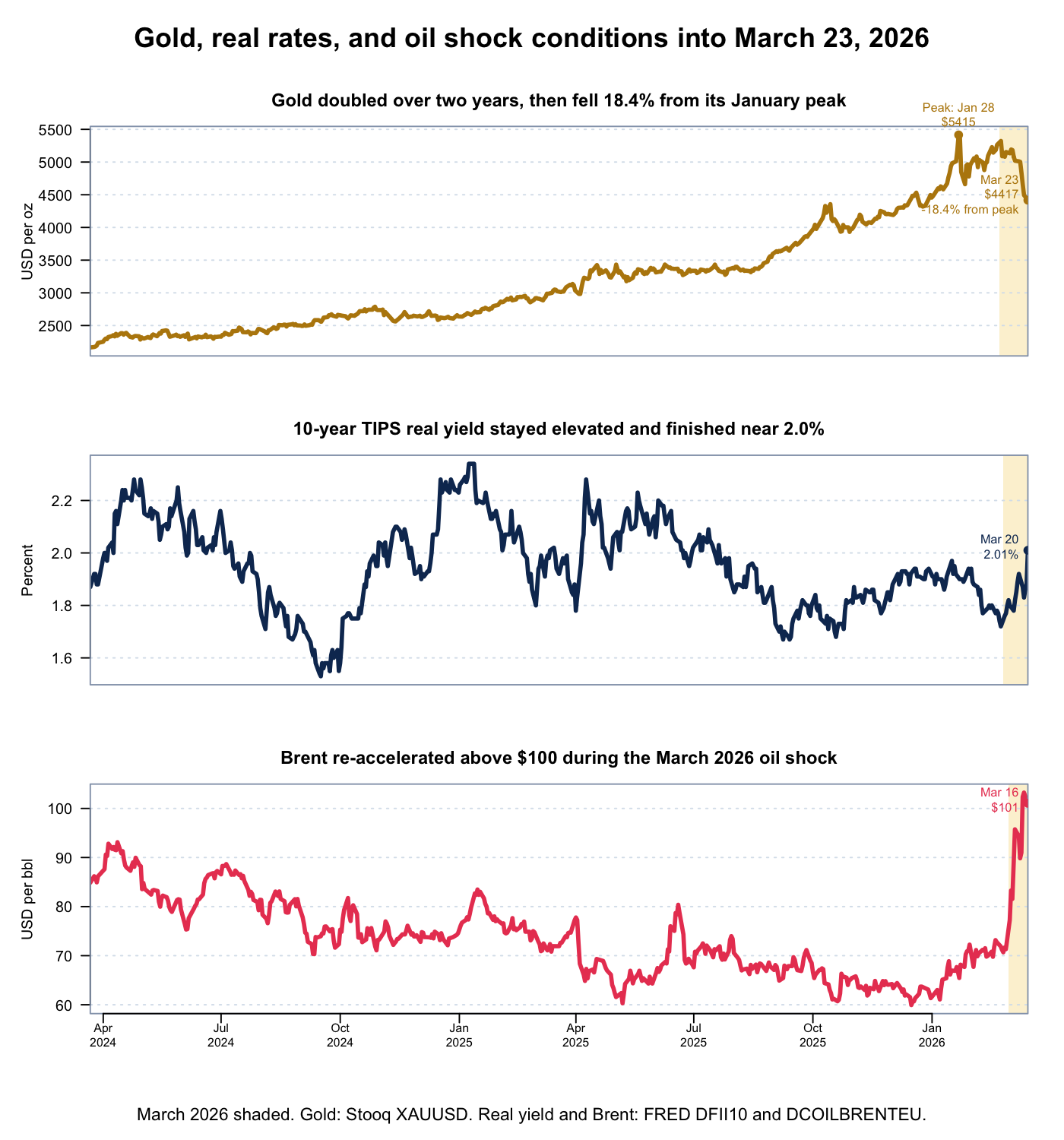

| Gold spot (Mar. 23, 2026) | $4,417/oz, up 104% from Mar. 22, 2024 | The move was already spectacular. Crowded trades get more fragile late in the run. |

| Gold drawdown from peak | -18.4% from the Jan. 28, 2026 high | That is not how a relaxed, structurally supported bull market usually feels. |

| 10-year TIPS real yield | 2.01% on Mar. 20, 2026 | Gold can cope with high real yields, but it usually rallies more easily when real yields are falling. |

| Brent crude | $101/bbl on Mar. 16, 2026 | Oil above $100 raises inflation pressure, but it can also reduce the room for rate cuts. |

Gold had a huge run, but real yields never truly collapsed and oil re-accelerated into March 2026. That is a less comfortable mix for bullion than the headline geopolitics alone might suggest.

Gold and real rates: the missing tailwind

One reason I am cautious here is that gold already performed brilliantly without getting the clean real-rate help a classic bull case would normally prefer. The World Gold Council has long highlighted how important the rates channel is for gold, especially over shorter horizons. Yet as of March 20, 2026, the 10-year TIPS real yield was still around 2.0%, not some crisis-level collapse in real returns.

That tells me two things at once. First, the rally was real and strong. Second, a lot of support came from other sources: geopolitical stress, reserve diversification, safe-haven positioning, and momentum. When a market rallies that far without its cleanest macro tailwind fully arriving, it can become more vulnerable once the narrative starts to wobble.

Why oil-shock inflation is different from monetary inflation

Investors often say "inflation is good for gold," but that statement is too loose. An oil shock is not the same as a broad monetary easing cycle. Supply-side inflation makes transportation, energy, and production more expensive. It can hurt growth while leaving policymakers reluctant to ease aggressively, because cutting too quickly risks validating the inflation impulse instead of offsetting it.

That matters because gold does best when the inflation backdrop comes with falling opportunity cost. If the market concludes that Brent above $100 means fewer cuts, later cuts, or stickier real rates, then the inflation headline is not bullish enough on its own. In that regime the metal is competing against elevated real yields instead of benefiting from their decline.

History helps sharpen the distinction. The oil shocks of 1973-74 and 1979-80 did not produce a single, mechanical gold response. Gold performed especially well in the late 1970s because inflation expectations were unanchored and real short rates were still near zero or negative before Volcker's tightening fully took hold. That is a very different regime from one in which oil is rising but 10-year real yields are still around 2%.

If your team has exposure to commodity shocks or policy-sensitive inflation

This is the kind of scenario work I do for clients in economic causal analysis and statistical consulting: quantify the risk, model the range of outcomes, and turn the macro story into something operational.

Are sharp gold drops a margin-call phenomenon?

This mechanism should be treated as a hypothesis rather than a settled fact. Even so, it is a plausible market-microstructure explanation for violent down gaps. When a liquid winner has doubled over two years and then begins to crack while funding conditions remain tight, investors often sell what they can sell, not what they most want to sell.

The latest CFTC positioning data make that story more nuanced. In the March 17, 2026 disaggregated futures-only report for COMEX gold, managed money held 130,147 long contracts against 28,104 short contracts, for a net long of roughly 102,000. That is meaningful, but it is not an obviously extreme speculative crowd: it sits roughly around the middle of the 2020-2026 range and well below the 215,000+ net-long peaks seen in late 2024 and January 2025.

That means the liquidation story should not be framed as a simple "too many longs got trapped" explanation. Gold is precisely the kind of asset that can become collateral for other bets: it is liquid, widely held, and easy to exit. A stressed tape can therefore still produce air-pocket declines through broader de-risking and collateral needs even when speculative futures positioning is not at a historical extreme. In other words, forced selling and macro repricing are not mutually exclusive; they often reinforce each other.

What would make me bullish on gold again?

For this process to reverse in a durable way, I would want to see some combination of the following:

A smaller oil premium would reduce the odds of sticky supply-side inflation.

A convincing rollover in 10-year TIPS would restore the cleanest macro tailwind for bullion.

Gold should stop cascading lower on stress days and start absorbing bad news more gracefully.

Put differently: gold probably needs less war premium in oil and more room for rate relief. That is a different setup from simply saying "there is inflation, therefore gold must go up."

FAQ: gold, real rates, and oil-shock inflation

Why is gold falling even with war?

Because war can raise oil and inflation without lowering real yields. If the market thinks the Fed has less room to ease, gold can lose one of its most important supports even while headlines look geopolitically bullish.

Is gold still a hedge against inflation?

Yes, but not every inflation episode helps equally. Gold generally responds better to inflation that coincides with falling real rates or easier policy than to inflation caused by a supply shock that keeps real yields elevated.

What would make gold rally again?

A calmer geopolitical backdrop, lower oil, softer real yields, and more stable price action would create a much healthier setup for a renewed bull leg.

Related Reading

- The Hormuz Crisis and the Price of Oil — a model-based look at how disrupted throughput affects Brent.

- Hormuz Duration Model: Day 19 Update — a duration-analysis view of how long the disruption could last.

- Statistical Consulting — custom models for markets, policy risk, demand shocks, and scenario analysis.

Data notes and sources

- Gold spot history (Stooq XAUUSD)

- 10-year Treasury Inflation-Indexed Security real yield (FRED DFII10)

- Brent crude spot price (FRED DCOILBRENTEU)

- CFTC disaggregated COMEX gold positioning report and historical compressed archives

- World Gold Council on gold and interest-rate sensitivity

- Richmond Fed discussion of late-1970s inflation, oil shocks, and real-rate policy